When you’re managing a chronic condition like rheumatoid arthritis or psoriasis, the cost of your medication shouldn’t be a barrier to treatment. But for many patients in the U.S., switching from a brand-name biologic to a cheaper biosimilar isn’t as simple as swapping pills. Even though biosimilars are FDA-approved, clinically equivalent, and cost up to 33% less, insurance companies often treat them the same way they treat the original drug-making the switch financially pointless.

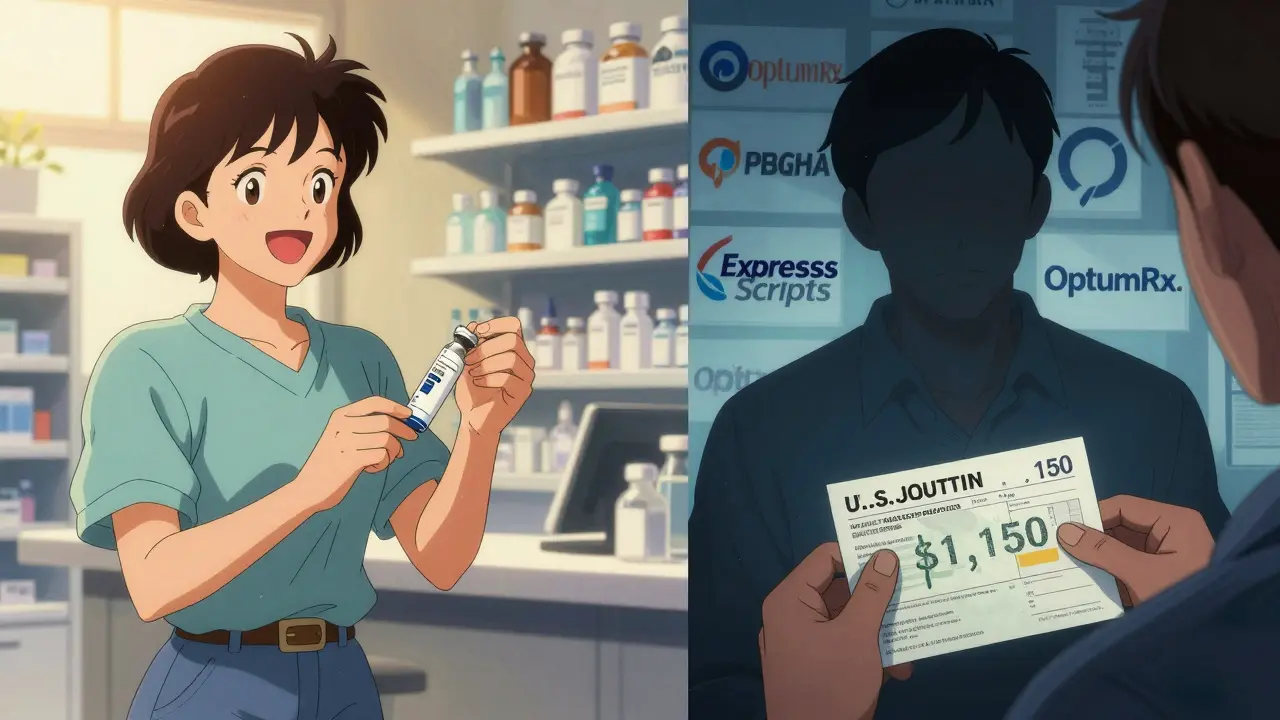

Take Humira, for example. It’s one of the most prescribed biologics in the country, with a list price around $5,000 per month. Eight biosimilar versions have hit the market since 2023, yet most insurance plans still place them on the same high-cost tier as Humira. That means if you’re on Medicare Part D or a private plan, your out-of-pocket cost for a biosimilar might be $1,150 a month-just $50 less than Humira. That’s not a savings. That’s a rounding error.

What Exactly Are Biosimilars?

Biosimilars aren’t generics. Generics are exact chemical copies of small-molecule drugs, like metformin or lisinopril. Biosimilars, on the other hand, are made from living cells-complex molecules that can’t be perfectly replicated. Think of it like a handmade sweater versus a factory-made one. They look nearly identical, feel the same, and do the same job, but the process to make them is wildly different.

The FDA approved the first U.S. biosimilar, Zarxio, in 2015. Since then, over 70 have been approved, though only about 40 are actually on the market. These drugs target conditions like cancer, autoimmune diseases, and diabetes. For instance, insulin biosimilars exist, but less than 10% of Medicare Part D plans cover them, even though over 80% cover the original Lantus.

The promise was simple: biosimilars would slash costs and open access. The Congressional Budget Office estimated they could save the U.S. healthcare system $54 billion over the next decade. But that only happens if patients can actually use them.

How Insurance Tier Systems Work

Most insurance plans use a tiered formulary system to control drug costs. Tier 1 is usually generic pills with a $10 copay. Tier 2 is brand-name pills with a $40 copay. But biologics? They’re almost always on Tier 4 or 5-the specialty tier. That means instead of a flat fee, you pay a percentage of the drug’s price. If your drug costs $5,000 and your plan charges 33% coinsurance, you’re paying $1,650 a month. Out of pocket. No cap. No help.

Here’s the catch: 99% of Medicare Part D plans put Humira and its biosimilars on the same tier. That’s according to the Department of Health and Human Services’ Office of Inspector General in late 2024. Not one plan gave biosimilars a better tier to nudge patients toward cheaper options. Even when a biosimilar is labeled “interchangeable”-meaning a pharmacist can swap it in without a doctor’s approval-only a few low-dose versions qualify. And even then, most pharmacies don’t even stock them.

Meanwhile, PBMs (pharmacy benefit managers) like Express Scripts, OptumRx, and CVS Caremark have started doing something more aggressive: they’re removing Humira entirely from their formularies. Not because they love biosimilars-but because they want to force patients into them. In 2025, Express Scripts excluded Humira from all its commercial plans. If you want the original, you have to appeal. But if you’re on a biosimilar? You get preferred status with lower coinsurance. It’s not about savings-it’s about control.

Prior Authorization: The Hidden Bureaucracy

Even if your plan covers a biosimilar, you still have to jump through hoops. Nearly all plans require prior authorization before you can get any biologic-brand or biosimilar. That means your doctor has to fill out paperwork proving you’ve tried other treatments first. For rheumatologists, this isn’t a quick form. It’s a 20-minute task, repeated for every patient. A 2024 survey found 78% of rheumatologists spend 3 to 5 hours a week just on prior auth requests.

And it gets worse. Many plans require step therapy. That means you have to try the biosimilar first-even if your doctor says it won’t work for you. One case from the Rheumatology Advisor described a patient with severe rheumatoid arthritis who waited 28 days to get her real medication because the plan forced her to try a biosimilar first. She lost muscle mass. Her pain got worse. She missed work. All because of a formulary rule.

Approval times vary. Some take 3 days. Others drag on for two weeks. If you’re on a tight timeline-say, you’re about to lose your job and your insurance-you’re stuck.

Why Don’t Plans Reward Biosimilars?

You’d think insurers would want to push cheaper drugs. But the system isn’t built for savings-it’s built for profit.

Pharmacy benefit managers negotiate rebates with drugmakers. The original biologic makers pay huge rebates to stay on formularies. If a biosimilar gets a better tier, those rebates disappear. So PBMs have no incentive to move patients toward biosimilars. In fact, they profit more when patients stay on expensive brands.

That’s why only 1.5% of plans put biosimilars on a lower tier. And why 98.5% of plans require the same prior authorization for biosimilars as for the original drug. The FTC called this out in 2023, saying these practices are anti-competitive. Former FDA Commissioner Dr. Scott Gottlieb said PBMs are creating “artificial barriers” that violate the intent of the law that created biosimilars in the first place.

Meanwhile, European countries have no such problem. In Germany and the UK, biosimilars make up over 80% of the market for drugs like Humira. Why? Because their systems are designed to reward cost savings-not rebates.

What’s Changing in 2025?

There’s a shift happening. CMS, the agency that runs Medicare, now requires insurers to report how they cover biosimilars. And they’re watching tier placement closely. In 2024, 78% of Medicare Part D plans included at least one biosimilar alongside the brand drug. That’s up from 62% in 2023.

Some PBMs are starting to make smarter moves. Express Scripts now places multiple adalimumab biosimilars on Tier 3-with 25% coinsurance instead of 33%. That’s a real discount. Patients on those plans could save $200-$400 a month. That’s life-changing for someone on a fixed income.

The Inflation Reduction Act gives CMS more power to enforce fair tiering. If a plan puts a biosimilar on a higher tier than the original, they could face penalties. That’s why analysts predict biosimilar market share will jump from 23% today to 40% by 2027. But it’s not guaranteed. It depends on whether regulators step in and stop the games.

What This Means for You

If you’re taking a biologic right now, here’s what you need to do:

- Check your plan’s formulary. Look up your drug and any biosimilars. Are they on the same tier?

- Call your insurer. Ask: “Is there a biosimilar for my drug? If so, what’s my out-of-pocket cost compared to the brand?”

- Ask your doctor: “Can we switch to a biosimilar? Will it require prior auth?”

- If your plan denies coverage, file an appeal. Use the FDA’s approval as your argument.

- Check if your drugmaker offers a patient assistance program. Some biosimilar makers now have copay cards.

Don’t assume your pharmacist can switch you. Even if a biosimilar is labeled “interchangeable,” many pharmacies won’t substitute without a doctor’s order. And even if they do, your plan might not cover the swap.

Where Do We Go From Here?

Biosimilars were meant to fix a broken system. They’re safe. They’re effective. They’re cheaper. But insurance rules are still stuck in the past.

Real change won’t come from patients begging. It won’t come from doctors writing letters. It will come when regulators force insurers to treat biosimilars like what they are: the same medicine, at a lower price. Until then, patients are stuck paying nearly full price for a drug that was designed to save them money.

The numbers don’t lie. The U.S. could save $5.3 billion a year by 2030 if biosimilars are used properly. Right now, we’re on track to save just $1.8 billion. That’s not a failure of science. That’s a failure of policy.

Are biosimilars as safe as brand-name biologics?

Yes. The FDA requires biosimilars to show no clinically meaningful differences from the original biologic in terms of safety, purity, and potency. Thousands of patients have used them in the U.S. and Europe with no increase in adverse events. The approval process is stricter than for generics.

Why don’t pharmacists automatically substitute interchangeable biosimilars?

Even though the FDA allows pharmacists to substitute interchangeable biosimilars without a doctor’s order, most don’t. This is because insurance plans often don’t cover the substitution unless the prescriber specifically writes for the biosimilar. Pharmacies also lack clear guidance on reimbursement rules, making substitution risky.

Can I switch from a brand-name biologic to a biosimilar mid-treatment?

Yes, but only if your doctor agrees and your insurer approves. Some patients switch successfully, especially if they’re experiencing high out-of-pocket costs. But if your plan requires step therapy, you may be forced to try the biosimilar first-even if your doctor says it’s not right for you.

Do all insurance plans cover biosimilars?

No. While most Medicare Part D plans now cover at least one biosimilar for Humira, many private plans still don’t. Insulin biosimilars are especially under-covered-less than 10% of plans include them. Coverage varies widely by insurer, state, and plan type.

How long does prior authorization take for biosimilars?

Typically 3 to 14 business days. Some urgent cases can be fast-tracked in 24-48 hours if your doctor marks it as time-sensitive. Delays are common, especially with complex conditions like autoimmune diseases. Always follow up with your doctor’s office if you haven’t heard back after a week.

What’s the difference between a biosimilar and a generic drug?

Generics are chemically identical copies of small-molecule drugs, like aspirin or statins. Biosimilars are made from living cells and are highly similar-but not identical-to their reference biologic. They require more complex manufacturing and testing. Both are cheaper than brand-name drugs, but biosimilars face more coverage barriers because of their complexity.

Is there financial help for patients switching to biosimilars?

Yes. Some biosimilar manufacturers offer copay assistance programs-similar to those from brand-name companies. You can also check with nonprofit organizations like the Patient Access Network Foundation or the HealthWell Foundation. Medicaid and Medicare Extra Help may also reduce your costs.

9 Comments

Insurance companies are literally profiting off people’s suffering. Biosimilars are FDA-approved, clinically identical, and cheaper-yet patients are still getting gouged. This isn’t healthcare. It’s a racket.

And don’t even get me started on PBMs. They’re not middlemen-they’re middlemen with a license to steal.

Wow. Just… wow. You laid this out like a courtroom closing argument-and I’m convinced.

Here’s the kicker: we’ve got 70+ approved biosimilars, but less than half are even on formularies. And when they are? They’re locked in the same tier as the $5K/month drug. That’s not a bug. It’s a feature.

Pharmacy benefit managers aren’t ‘managing benefits’-they’re managing profits. And patients? We’re just line items.

Also-interchangeable biosimilars? Pharmacists won’t swap them because the system doesn’t pay them to. So even when the science says ‘yes,’ the bureaucracy says ‘no.’

It’s like buying a Tesla and being told you can’t drive it unless you pay the same price as the gas-guzzler you’re replacing. And then the dealer says, ‘But it’s technically the same car.’

Insane. And it’s all legal.

The structural disincentives embedded within the PBM-biopharma rebate ecosystem are not merely suboptimal-they are perniciously misaligned with both clinical efficacy and cost-containment imperatives.

By maintaining identical tiering for biosimilars vis-à-vis originator biologics, payers effectively nullify the intended price elasticity of substitution, thereby perpetuating rent-seeking behavior by incumbent manufacturers.

Moreover, the absence of mandatory formulary preferencing-despite statutory authorization under the Biologics Price Competition and Innovation Act-constitutes a regulatory failure of monumental proportions.

The Congressional Budget Office’s $54B ten-year projection remains theoretical, as the current incentive structure rewards non-substitution. The FTC’s 2023 findings are not merely indicative-they are damning.

Comparative regulatory frameworks in Germany and the UK demonstrate that market-driven biosimilar uptake is achievable through transparent, non-rebate-dependent pricing mechanisms. The U.S. model is not an outlier-it is a distortion.

Until CMS enforces tier parity and mandates reimbursement parity for interchangeable agents, the biosimilar revolution remains a policy mirage.

And yes-the fact that pharmacists are legally permitted to substitute but financially disincentivized to do so is a grotesque institutional contradiction. It is not incompetence. It is design.

My sister’s on Humira. Switched to a biosimilar last year. Her copay dropped from $1,200 to $900. Still too much. But at least it’s something.

She had to fight for 3 months to get it approved. Her doctor spent 10 hours on paperwork. No one helped. No one cared.

Just saying-it’s real. And it’s happening to people you know.

Let’s not forget the systemic inertia at play here. The biologic manufacturers don’t just pay rebates-they pay for exclusive contracts, advisory boards, patient advocacy groups, and even continuing medical education for physicians. The entire ecosystem is built around locking in the high-price product.

Biosimilars didn’t just come into a vacuum-they came into a fortress.

And now, when PBMs exclude Humira from formularies, they’re not doing it out of altruism. They’re doing it because the biosimilar maker offered a *better* rebate. So now, instead of paying $5,000 for Humira, you pay $4,800 for the biosimilar-and the PBM pockets the difference. The patient still pays 33%. The system still wins.

It’s not about cost. It’s about who gets the cut.

The only way forward is to ban rebate-based formulary placement. Period. If a drug is clinically equivalent, it must be on the same tier with the same out-of-pocket cost. No exceptions. No loopholes.

And yes, the FDA’s approval should be enough. If we trust biosimilars to be safe, why don’t we trust them to be affordable? The answer: because profit > principle.

As a rheumatology nurse practitioner, I see this daily. A patient on Humira with a $1,500 monthly copay. Biosimilar available. Same efficacy. Same side effect profile. But the plan requires prior auth, step therapy, and a 14-day wait.

I had one patient delay treatment for six weeks because her plan insisted she try the biosimilar first-even though she’d been stable on Humira for 8 years. She developed a severe infection. Lost her job. Had to go on disability.

It’s not just inconvenient. It’s dangerous.

And when we appeal? The insurer says, ‘We follow FDA guidelines.’

Then why won’t they cover the biosimilar the same way?

Because guidelines don’t pay rebates.

Policy needs to catch up to science. And fast.

It’s not just the U.S. that’s broken. It’s the entire model. In Europe, biosimilars are the default. No prior auth. No tier games. No PBM shenanigans.

Here, we’ve turned healthcare into a corporate chess game where patients are pawns.

The fact that we still debate whether biosimilars are ‘equivalent’ is a scandal. They’re not generics. They’re not the same. But they’re close enough to save lives-and we’re still making people beg for them.

And don’t tell me about ‘market forces.’ This isn’t a market. It’s a monopoly with a side of fraud.

man i just read this whole thing and im like… why is this so complicated? i mean, if its the same medicine, just cheaper, why cant we just use it? like, my cousin got a biosimilar and her bill went from 1300 to 800 a month. not perfect but way better.

also, why do doctors have to fill out 1000 forms? i get it, insurance is a mess, but this feels like a glitch in the matrix.

ps: i think the word 'biosimilar' should be in the name of the drug so people know its not some weird new thing. just sayin'.

As someone who grew up in India and now lives in the U.S., I’ve seen both systems. In India, biosimilars are the standard. No prior auth. No tiered formularies. No PBM middlemen. Just a doctor’s prescription and a pharmacy that stocks it.

Here? We’ve turned a medical innovation into a bureaucratic obstacle course.

The irony? The U.S. invented biologics. The U.S. approved biosimilars. But we’re the only country that’s made them harder to access than the original.

It’s not a failure of science. It’s a failure of will.

And the worst part? We have the power to fix this. We just don’t have the courage.

Maybe next time someone says ‘America leads the world in innovation,’ we should ask: ‘Innovation in what? Profit? Or patient care?’